TJ Agresti, JD, LLM, CAMFounder and President Archives

February 2021

|

Back to Blog

Cash Is King But Don't Be A Sucker5/28/2020  Private Investors Have An Abundance of Cash and Want to Invest Business Finance | 3 Min Read Warren Buffett famously said, “Be fearful when others are greedy, and be greedy only when others are fearful.” After the Federal government's rescue of the economy avoided a complete collapse of the capital markets during the last Great Recession there was an abundance of greedy investor capital looking for devalued businesses to invest in or acquire outright. New research from the JP Morgan Chase Institute finds that many small businesses are living month to month, and the median small business has only enough cash in the bank to last 27 days without additional funds. "It is well known that small businesses are a critical driver of economic growth, but the consistency of their growth is in question if they're living month to month," Diana Farrell, president and CEO of the JP Morgan Chase Institute, said in a statement. Now, it's becoming apparent that the amount of cash sitting on the sidelines waiting for the right moment is even larger than the last time. The targets will be your stressed business that may be running out of cash.

While we still do not know the depths our economy may go to during this "Great Social Distancing" we do know that the government will do whatever is necessary to avoid depression like economics and provide an opportunity for a swift recovery. At least that is the intent otherwise 22 million unemployed Americans and counting don't go back to work. We end up with 10% plus persistent unemployment, an enormous national debt and a stagnated economy creating the real possibility of sovereign debt default or a currency devaluation event (but this is another topic). Whether the current stimulus package will succeed or not is yet to be seen but there is enough support for a vaccine within a year and therapeutic treatment before that to create optimism for a faster than normal recovery from the depths of the current crisis. Now is the time to engineer your financial plan for the recovery using income models based on the best case of rapid recovery, the worst case of extended recovery and something in the middle that resembles a start stop approach to the recovery of economic activity. The intermittent activity model accounts for the likelihood of waves of social distancing that might occur until a widely available vaccine or therapeutic drug is available. A key part of the financial plan is a supportable stock valuation model that will be the basis for any negotiation with a private investor. Valuation is the determining factor of percentage ownership you have to give up to get the capital you need to support your recovery business model. Additionally, private investors want a clear picture of how they get their capital back with a multiple of yield over a given period of time. You must have a viable exit strategy built into your financial model which tracks the valuation adjustment over time as your business recovers and grows. The realization event for the new valuation may be a merger, sale or IPO. Private capital is available to rescue your company and support a relaunch but don't be taken advantage of by a lack of preparation. Questions to Ask

1 Comment

Back to Blog

Business Finance | 5 Min Read  SBA Extends PPP Loan Safe Harbor. Forgivable Money Still Available Uncertainty Abounds

Over the past several weeks, the SBA's and Treasury's uneven administration and rules guidance of the PPP, created a large amount of uncertainty for many businesses who already applied for and obtained their loan proceeds. A series of rule changes, guidance and press releases by the SBA and Treasury have many businesses giving back their PPP Loan proceeds out of fear they no longer qualify and may be subject to criminal prosecution. Many other businesses are reluctant to even apply for PPP loans due to the perceived risks. Borrowers Frustrated Borrowers report requirements are challenging to either comply with or to meet in order to qualify for maximum loan forgiveness. Nearly half they say using the loan within the eight-week window is somewhat or very difficult, and the same percentage finds it very or somewhat difficult to get employee headcount back to pre-crisis levels. New guidance issued May 13, meant to relieve PPP loan recipients confusion and anxiety, is being met with broad relief from PPP participants and potential applicants who may be sitting on the fence, and is available from the SBA at PAYCHECK PROTECTION PROGRAM LOANS Frequently Asked Questions (FAQs) and from the US Treasury website at PAYCHECK PROTECTION PROGRAM LOANS. Treasury/SBA Update There are a 47 questions and answers providing updates and clarifications from the SBA. The top changes with the greatest potential impact are:

Owner Questions Business owners have questions about how to spend the funds and what they can spend the loan on as many of the terms and conditions are broad and unclear when applied to specific business operations. "Nearly three-fourths of small business borrowers find the terms and conditions of the PPP loan difficult to understand with 22% finding them very difficult,” the SBA report said. While many PPP participants are relieved about the guidance, there is still significant apprehension that additional changes may occur resulting in unexpected non-compliance by businesses who are attempting to act in good faith. As a result, many advisors, including Critical Mission Consulting, Inc., a Denver business consulting firm, are counseling a conservative wait and see approach, when possible. What To Do Critical Mission Consulting, Inc. President, T.J. Agresti, sad about their business clients, "there is nothing that requires businesses to spend their PPP proceeds immediately. We are telling businesses, especially those planning to request loan forgiveness, to hold off on spending their loan proceeds and to wait as long as possible within the 8 week loan forgiveness period." Main Street advocates are eager to see lawmakers move ahead with proposed changes when the House votes on the Paycheck Protection Flexibility Act, which makes tweaks to the PPP, including extending the covered-period window of eight weeks and the split on what the funds can be used on. The proposed changes have bipartisan support and could encourage more business owners to apply for aid. “No doubt, these key changes will make the program work more effectively for small businesses and their employees. These changes also align with conditions on the ground,” said Karen Kerrigan, president and CEO of the Small Business & Entrepreneurship Council. “PPP needs to be structured more flexibly at this point given the very different stay-at-home and shutdown orders in the states, and the very different plans and phases for re-openings, which will drive demand,” she said. “A one-size-fits-all PPP program does not work — things have changed tremendously since the design of the program in early to mid-March.” However, some business have no choice but to spend their PPP loan proceeds to keep their business afloat. "We are advising our clients to spend 75% on payroll qualifying expenses but if its between losing your business or having to repay the PPP loan, then do what needs to be done and save your business," said Mr. Agresti. These business have no choice but to ride out the uncertainty surrounding guidance of the PPP and hope they are compliant with the final rules. There is momentum to make the program more flexible and the addition of the safe harbor should cover the vast majority of borrowers. Businesses who accepted under $2 million covers over 98% of Phase One loans and over 99% of Phase Two loans according to the SBA. The risks associated with taking a PPP loan may now be acceptable for many more businesses who were in a holding pattern waiting to spend their loan proceeds or apply for a new loan. Money Still Available There is still an opportunity to apply for and receive forgivable loans from PPP. The program has $126.5 billion in funding left, according to the Small Business Administration. A careful review, with advisors, of the application requirements, and the rules on how to obtain forgiveness, if that is the goal, are a must. Forgiveness is available if you use 75% of the loan for payroll but even if you don't want forgiveness, the loan is still inexpensive capital with a 2 year term and an interest rate of 1%. For more news and reporting on the coronavirus and how businesses can handle challenges related to the Paycheck Protection Program and the pandemic, visit T.J.'s blog page or go to the Critical Mission Consulting website Coronavirus resources page.

Back to Blog

Business Finance | 9 MIN Read  You're leading in a crisis and need a loan for working capital. What can you do to improve your odds? Loan Repayment Insurance Is The SecretThe ability of a business to borrow money will make the difference between surviving or failing during the current crisis and being ready to thrive when the economy recovers. Many business leaders are asking their advisors for guidance on how to improve their odds of successfully obtaining a loan. At the same time, lenders are looking at the economic landscape trying to navigate a level of unprecedented uncertainty which is creating barriers to lending. A new lending product has emerged to provide both lender and borrower assurance that a loan will be repaid during these uncertain times. It’s called Performance Guarantee Insurance. Performance Guarantee Insurance is coverage that guarantees the borrower's repayment of a loan. It affords companies the best chance at getting the working capital needed to survive, move forward, and be prepared to grow again as the economy comes to life and recovers. Lenders see a highly rated insurance company standing behind the borrower as the deciding factor in approving the loan. These are tough times that require tough decisions by business leaders who are making every effort and taking every action necessary to insure the continuing viability of their businesses. Unprecedented Times The economic damage is triggering comparisons to the Great Depression. The economic activity of the U.S. continues to plummet during the corona virus pandemic. Unemployment is soaring because of stay at home orders, social distancing policies and disruptions in supply chains due to outbreaks at critical production facilities. As a result, the US economy has shed 33.5 million jobs through May 7. This is not a typical “black swan” event with the depth and speed of the economic decline exceeding that of the Great Depression. To put the economic impact in perspective, at the beginning of March 2020, the unemployment rate was 4.4% - what many economists consider a natural rate of unemployment. Now, that "real" rate has blown up to 24.7% unemployment and we are facing the reality that unemployment could rise above the Great Depression high of 24.9% to 30%, according to reports from the Federal Reserve Bank of St. Louis, with a contraction of GDP exceeding 38%. This impact would be worse than the Great Depression since unemployment is a lagging indicator of economic activity. Employers resist hiring new employees until there is confidence the economy will rebound and stay strong. It’s clear businesses are looking at continued suffering. The need for additional working capital will continue to increase as the depth of the economic downturn deepens and the recovery is prolonged. Long Recovery Cash flow plans need to account for the uncertainty of how long a recovery might take Businesses are suffering unprecedented declines in revenue while at the same time the risk to their operations’ long-term viability grows. The risks for the economic recovery are severe, with many economists indicating the recovery is likely to be a long and grueling process that could take three or more years with severe ups and downs along the way. As businesses struggle to survive the current shock, they need immediate cash in the form of loans and refinanced debt. Of critical importance to both the borrowing company and the lender is the risk of repayment. Naturally, in this climate, the higher the probability of default on a loan may result in no loan at all. Even if loans are considered, they may come with terms too costly for the borrower. The little-known secret of Performance Guarantee Insurance reduces the repayment risk for the borrower and the lender. As a result, the likelihood a loan will be approved is greatly increased. Of course, it remains a tough decision for a business to take on new debt or refinance its existing debt. Tough Times Require Tough Choices To lead in a crisis means making tough choices to assure the long-term viability of the company. Businesses in every industry are making tough decisions warranted by a crisis of the magnitude that COVID-19 represents. It started with furloughs and pay cuts, but every aspect of operational costs is being analyzed for possible savings, all with a focus on understanding how much cash the business will need and for how long. This is only part of the equation. All businesses need to ensure their financing remains viable. The process requires scenario based planning and a critical self-assessment of a business’s ability to service the debt. Debt refinancing is a critical step in the cash flow analysis process. It can strengthen net positive cash flow and slow the burn rate to buy critical time until a recovery begins. Refinancing is a simple concept to pay down remaining debt from a loan with proceeds of a new loan with better terms, including more money for working capital, longer repayment terms, lower rates, and less frequent payments. However, the financial analysis of whether to refinance or not is more complex as the lower payments may come with a lot of potential negatives. Debt refinancing means paying interest on interest. Prepayment penalties may be triggered. Refinancing short-term debt with other short-term debt can get very expensive creating a cash flow cycle from which a company cannot successfully emerge. The decision to take on additional debt may seem simple on its face, balanced against the need for working capital in the midst of a sudden downturn in revenues. Again, the simple is not so obvious when considering the ability to repay the new loan must consider various projected cash flow models from optimistic to worst case scenario. All of these factors pit a borrower’s hunger for funds and repayment risk profile against the lender's risk tolerance appetite. What’s needed is a financial structure that transfers the repayment risk, improves the risk profile for the borrower and increases the risk appetite for the lender. Performance Guarantee Insurance satisfies the needs of both the borrower and lender with an insurance contract guarantee for the repayment of the loan. The use of insurance allows a contractual structure, backed by a highly rated insurance company, that is familiar to business operators and lenders. Insurance Transfers Risk Risk management often includes insurance to transfer the risk to an insurance company. Risk transfer using insurance is an integral component to an effective risk management plan. Insurance, at its core, is about transferring a defined risk of loss from one party to another in exchange for a premium. The premium represents the cost to cover the risk associated with a contractual obligation to pay a benefit in the event the defined risk occurs. In the case of life insurance, the premium an individual pays covers the costs of the insurance company having to pay a benefit in the event of death. The costs of coverage for any risk require people called actuaries, who work for insurance companies to determine the risks associated with a policy. They look at how likely an event like death, disaster or an accident is, and the likelihood of a claim being filed, as well as how much the company will be on the hook for paying out if a claim is filed. They put this information into a chart called an actuary table and give this to a person called an underwriter. Now, the underwriter uses this data along with information provided by the person or company asking for insurance when they issue a policy to determine what the exact premium will be for coverage they want. Insuring The Loan Repayment An insurance policy can guarantee repayment of a loan to the lender in the event of borrower's default. Almost any risk can be quantified by insurance actuaries, including the risk that a borrower will default on a loan over a given time period due to a lack of revenue. Numerous factors are considered when actuaries quantify the risk of a borrower defaulting on a loan. Some of these are the macroeconomic conditions, specific borrower strengths, weaknesses, opportunities, and threats, current industry conditions, operational risks, revenue risks, current asset valuation and supply chain risks. Today, the duration of the pandemic with possible ebbs and flows over time are a new factor. The actuaries consider all these factors to create an actuary table indicating how likely it is that a borrower will default on a loan and how much the insurance company will have to pay if a claim is filed. The underwriters use the actuary table along with additional information on the company and/or the individual owners of the company to determine what the exact one-time premium will be to insure the repayment of the loan i nth event the borrower defaults. The total loss guarantee on the loan is straightforward to measure based on the loan principal, interest, and penalties in the event of a default at a given time in the life of the loan. Naturally, the insurance is only as good as the strength of the company standing behind the promise to repay the loan, as indicated by their credit rating. The Promise Behind Insurance

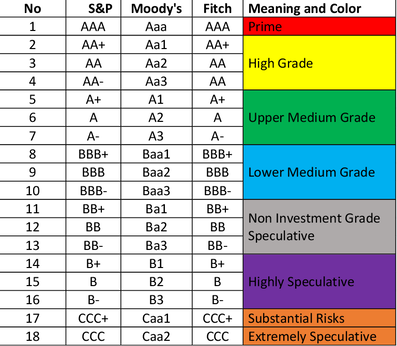

Borrowers and lenders relying on the promise of an insurance company to pay off a loan in the event of a default will prefer, or even demand, an insurance company with an investment grade rating to issue the Performance Guarantee Insurance. An investment grade rating provides the assurance that the insurance company will be able to meet its obligation to pay the benefit in the event the borrower defaults on the loan. As an example, an insurance company with an S&P Global rating of 'AAA' has the highest rating assigned by S&P Global Ratings. The obligor's capacity to meet its financial commitments on the obligation is extremely strong. An insurance company rated 'AA' differs from the highest-rated AAA only to a small degree. The obligor's capacity to meet its financial commitments on the obligation is very strong. In the case of Performance Guarantee Insurance, the issuing insurance company has a 'AA' S & P Global Ratings which indicates the insurance company's solvency, financial strength, and ability to pay policyholder claims is very strong. The borrowers and lenders can be confident the loan will be repaid because of the capacity and willingness of the insurance company to meet its financial commitments on the Performance Guarantee Insurance in accordance with the terms of the insurance contract in the event of a default. Best Odds For A Loan Approval Performance Guarantee Insurance can make the difference in getting a loan approved. Shifting the risk that cash flow will not be sufficient to repay a loan from the borrower to an AA rated insurance company is a powerful tool to improving the odds of a loan getting approved. The risk profile of the borrower is drastically improved based on the investment grade guarantee behind the borrower’s performance. The back stop of the insurance creates the financial strength of a stabilized projected revenue stream and a balance sheet protection. The final result is improved credit worthiness and an attractive loan for the lender. In fact, the financial impact of Performance Guarantee Insurance may allow a company to obtain their own investment grade rating of BBB or better. An investment grade rating is especially important for companies seeking to offer their own debt for sale in the form of bonds. Lenders, as the beneficiaries to the coverage, mitigate their downside risks associated with potential poor financial performance for their existing and future loan portfolios. A lower risk profile often results in better loan terms that are more cash flow efficient for the borrower further strengthening the outlook on the borrower’s performance long term. Bottom LineThere’s great uncertainty about jobs and the economy, about the federal SBA and PPP loans, and about reopening businesses and the potential for closing them again later in the year. Performance Guarantee Insurance enables both small and large businesses to engage lenders and acquire much needed cash. The insurance increases the likelihood of borrowing success by improving the creditworthiness of the borrower thereby reducing the risk for lenders. This is a great message to send to internal and external stakeholders, as well as lenders who want to help businesses survive these unprecedented times. Disclaimer: Critical Mission Consulting, LLC is providing Performance Guarantee Insurance to its customers.

|

RSS Feed

RSS Feed

|

Privacy Policy

Cookies policy Terms of Use Disclaimers © 2013 - 2024 Critical Mission Consulting LLC All Rights reserved |